Stop Hunting on Crypto Exchanges: Front-Running, Spoofing, and Why Retail Traders Keep Losing

Forbes chose their headline carefully: "Fish in a Tank with Sharks."

The image is precise. Stop hunting on crypto exchanges is not a glitch or a market anomaly. It is the rational exploitation of visible order placement on a transparent order book, and it happens every day to retail traders who do not know the architecture they are trading on.

On a central limit order book (CLOB) exchange, your stop-loss orders, position sizes, and entry prices are visible to any participant sophisticated enough to read the book. The market maker across the ledger has co-located servers, real-time analytics, and capital that dwarfs the average retail account. You are not competing. You are occupying different trophic levels of the same ecosystem.

This is not a metaphor. It is a structural description of how most crypto exchanges are built, and why stop hunting, front-running, and spoofing are not exceptions on those platforms. They are features of the architecture.

This article breaks down each mechanism in plain language: what it is, how it works on a CLOB, and why the No-CLOB model eliminates each one by design.

The Structure Problem, Not the Ethics Problem

Most discussions of stop hunting, front-running, and spoofing frame them as ethical failures. Bad actors doing bad things. That framing is incomplete.

The structural version of the argument is more useful: these practices exist because the exchange architecture that most platforms use makes them possible, profitable, and difficult to detect or prove. Bad actors are opportunistic. The CLOB gave them the opportunity.

A transparent public order book is a democratizing mechanism. Any market participant can see the same information. The information advantage that professionals hold in traditional finance, proprietary order flow, dark pools, institutional routing, is supposed to be visible on a CLOB. In theory, you see the same book as the market maker.

The problem is that seeing the same data is not the same as having the same capacity to act on it. The market maker has co-located servers and algorithmic execution measured in microseconds. You have a browser tab. The CLOB produces equal information access and a radically unequal ability to exploit it.

Stop Hunting on Crypto Exchanges: Why Your Stop-Loss Is a Target

A stop-loss order is a risk management tool. You open a trade, set the maximum loss you are willing to accept, and place a stop-loss at that price. If the market reaches that level, your position closes automatically.

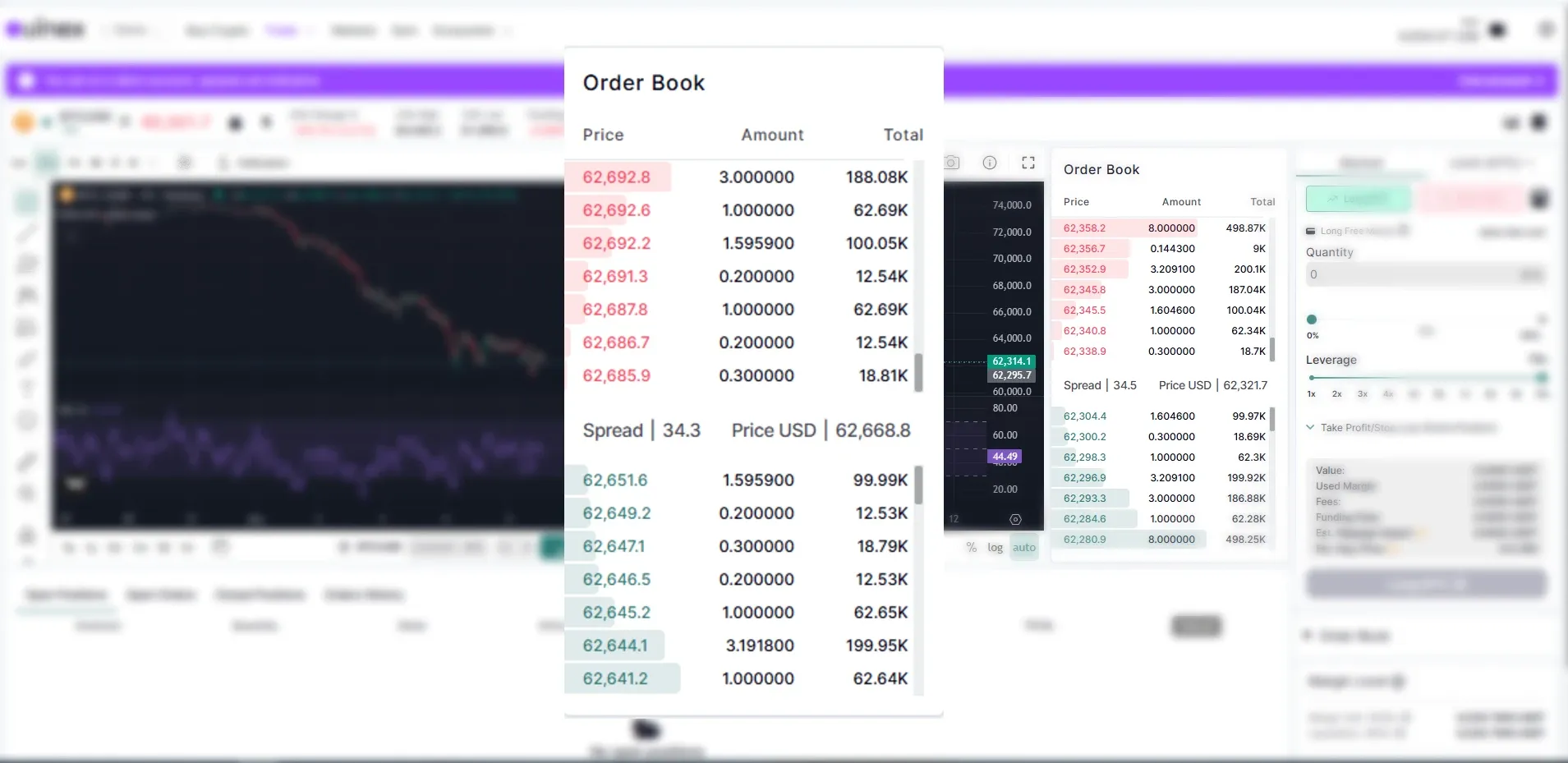

On a CLOB, those orders are visible.

Market makers and sophisticated participants can read the distribution of stop-loss orders clustered below key support levels. They know, with high precision, where you have placed your exits. A coordinated sell into that zone pushes price through the stop cluster, triggering a cascade of automatic closes. The triggered orders drive prices further down. The initiating participant buys back at the lower price.

Your stop-loss executed as intended. The position closed at the predetermined level. But the price move that triggered it was engineered, not organic.

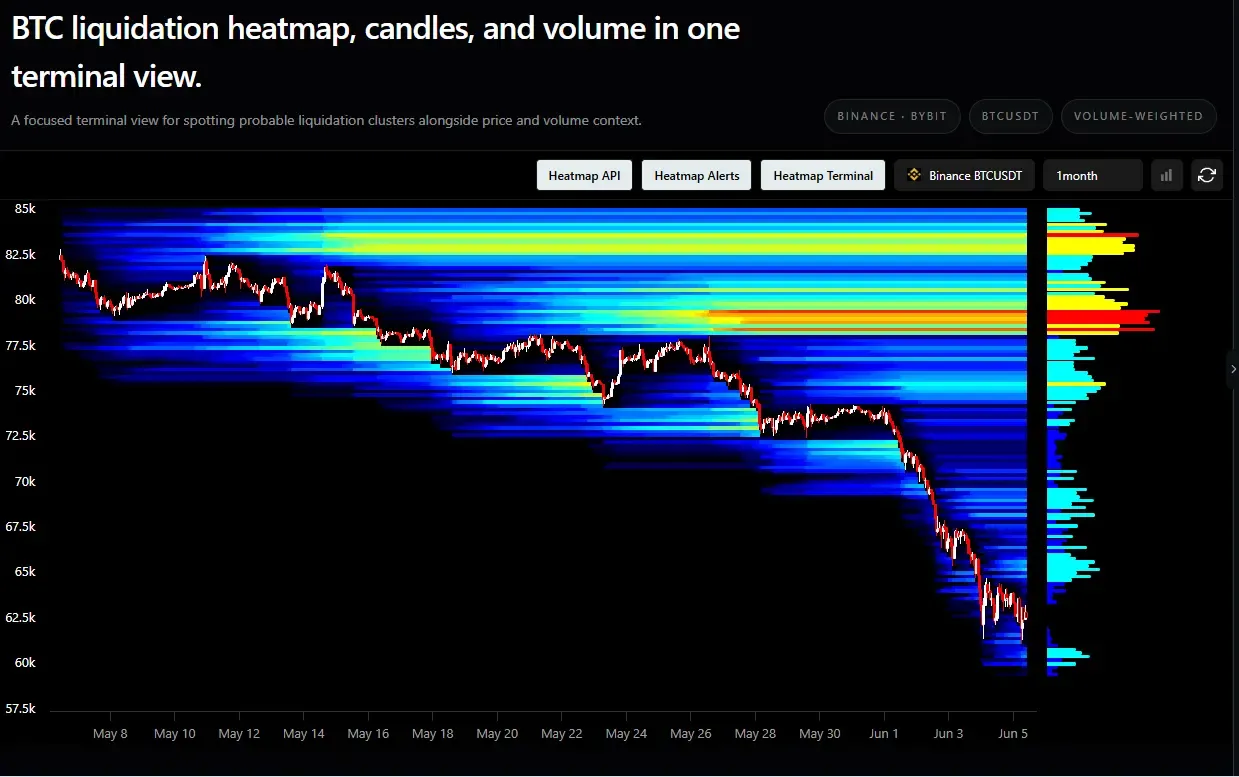

Example of a stop hunting behavior.

Another example, imagine you hold a BTC long, you place stop-loss at the recent swing low. It is a technically obvious level that other traders would also use. Price drifts toward that level, accelerates through it, triggers stops across the book, then reverses within minutes. You are out. The market maker is long.

This is to stop hunting on a crypto exchange: the structural edge that disappears when the order book is not visible. In a No-CLOB model, there are no stop-loss clusters to read.

Front Running on Crypto Exchanges: The Speed Asymmetry

"A retail trader in a Starbucks with a phone competes on the same book as a market-making firm with 20 employees and a few million in capital." - Boaz Sobrado, Forbes

Front running on a crypto exchange is what happens when that asymmetry interacts with order book transparency.

When a large market order is incoming, the kind that will move price, a market maker with faster infrastructure can detect it before it executes, position ahead of it, and exit after the price impact occurs. Your order moves the market. The market maker profits from that movement.

The mechanism requires two conditions: visibility into incoming order flow, and the ability to act faster than the originating trade. On most CLOB exchanges, both are met. The order book is public. Professional participants have infrastructure designed to read it and respond in microseconds.

The result is that a retail market order on a CLOB is not just an execution. It is a signal immediately acted on by faster participants. You pay the market maker to front-run you, through the spread and price impact of every large trade.

Crypto Exchange Spoofing: The Order That Was Never Real

Spoofing is the placement of large orders with no intention of executing them.

The purpose is to create the appearance of demand or supply. A large buy order placed below market suggests support. Other participants read it as institutional interest and trade accordingly. When those participants have positioned in the direction the fake order implies, the spoofer cancels the order and trades the opposite direction into the momentum they created.

The distinguishing feature from stop hunting is intent: crypto exchange spoofing requires placing an order you plan to cancel before it executes. On most CLOB platforms, cancellation is essentially free. There is no structural cost to placing a misleading order, allowing it to influence other participants, and removing it before execution.

Regulators in traditional finance treat spoofing as illegal order book manipulation. In crypto, enforcement has been inconsistent. The more fundamental point is structural: on a CLOB, spoofing is technically trivial and detection is retrospective, not preventive. Policy cannot run faster than the mechanism.

What a No-CLOB Exchange Changes: Ouinex.

The No-CLOB architecture does not rely on policy to prevent these practices. It removes the structural conditions that make them possible.

"On most platforms, market makers can see the order book and position against retail traders. On ours, it stays hidden from them." - Samuel Rondot, Head of Trading at Ouinex, BeInCrypto

Three structural shifts follow from a hidden order book:

No visible stop-loss clusters.

Without that visibility, stop hunting requires guessing rather than reading. The structural edge disappears.

No visible order flow.

The information a market maker would use to detect and position ahead of an incoming order simply does not exist. Your order executes against the platform's liquidity model without being observable in advance.

No audience for spoofing.

Spoofing requires a public book to manipulate. If the order book is not visible to other participants, placing large fake orders has no effect. The incentive structure for order book manipulation is eliminated at the root.

This is not a claim that a no-CLOB exchange is fraud-proof in every imaginable dimension. It is a claim about mechanism: the specific structural conditions that enable stop hunting, front running, and crypto exchange spoofing on a CLOB do not exist in a No-CLOB model. The elimination is architectural.

Why the Exchange's Funding Model Matters

There is a second-order point worth making, and Forbes made it.

A CLOB-based exchange that allows stop hunting and front running benefits from the volume those practices generate. The incentive to eliminate them competes directly with the incentive to maintain transaction revenue. When the exchange is funded by institutional capital with return timelines, the structural reform that benefits retail traders also reduces revenue. That creates a structural reason to delay it.

Ouinex was funded by more than 10,000 retail and professional traders: $9 million raised without institutional capital. As TheStreet reported, the exchange's shareholders are its users. The people who own the platform are the same people who would be harmed by a CLOB architecture. That alignment is not incidental to the No-CLOB design. It is the reason the design exists.

The Practical Implication

Most retail traders have lost money in situations they attributed to bad luck or poor timing. Some of it was. Some of it was to stop hunting. Some of it was a market order that executed into a front-run they did not see coming.

The distinction matters not for assigning blame but for making accurate decisions about where to trade. If the architecture of the exchange you use makes these practices possible, the cost shows up in execution quality, not in a line item.

The crypto perpetual futures on Ouinex operate under the No-CLOB model. The safety of assets framework covers how the platform handles custody and segregation. The full breakdown of what this means in practice is on the Ouinex Advantage page.

The structure is the product. Understanding what it eliminates is the same as understanding what you are actually trading on.

FAQ: Stop Hunting and Order Book Manipulation Explained

What is stop hunting on a crypto exchange?

Stop hunting on a crypto exchange is when sophisticated participants deliberately push price into zones where retail stop-loss orders are clustered, triggering a cascade of automated position closes. The price then reverses, leaving retail traders out at the worst moment. It is possible on CLOB exchanges because stop-loss order placement is visible in the public order book.

How does front running work on a crypto exchange?

Front running on a crypto exchange happens when a participant with faster infrastructure detects an incoming large order before it executes and positions ahead of it. When the original order executes and moves the price, the front-runner profits from that movement. It requires two conditions: visibility into the order book, and the ability to act faster than the originating trade. Both conditions exist on most CLOB exchanges.

What is spoofing on a crypto exchange?

Crypto exchange spoofing is the placement of large buy or sell orders with no intention of executing them, designed to create a false impression of demand or supply. The spoofer cancels the fake order once other participants have repositioned, then trades the opposite direction. It is a form of order book manipulation that is structurally difficult to prevent on CLOB platforms because cancellations are free.

What is a No-CLOB exchange?

A No-CLOB exchange does not use a central limit order book. Instead of a public ledger where all bids and asks are visible, the order flow and book remain hidden from participants. This structurally eliminates the conditions required for stop hunting, front running, and spoofing on crypto exchanges, because the information those practices depend on is not available.

How can I trade on an exchange without stop hunting or front running?

Trading on an exchange without stop hunting requires choosing a platform that removes the structural conditions enabling these practices. A No-CLOB exchange eliminates the visible order book that makes stop hunting and front running possible. On CLOB-based platforms, placing stops away from obvious technical levels reduces exposure, but this is a tactical workaround to an architectural problem. The only structural solution is an exchange without front running and without a visible order book.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.